Appartment #1 (Contract #1)This is what my partner (dad), had to say about this property from the beginning...

Here's my story, it's sad but true...

Everyone knows that you should hold real estate in an LLC. So, in an effort to get started out right, my son and I decided that we should set up that LLC. With some help from the company I work for, we set up our LLC by ourselves. The cost to set one up in NY was $200. In addition, I spent $26.95 for a downloadable Operating Agreement that I modified to fit our needs, plus about $70 for the required advertising and affidavits.

Problem one arises. Did you know that if you start an LLC in NY in 2005, but don’t actually buy a property, you still have to pay a $500 annual fee? Lesson #1: Don’t form the LLC until you at least have a property in mind.

I went home invigorated after the Rich Dad Poor Dad Meeting 2006 in Scottsdale, AZ. We tracked down a few realtors and found two that I like. One Realtor, Lisa, looks for multi-family homes for us. The other, Greg, deals in REO’s and “as-is” homes. In addition, we hired one of my son’s college friends to print and mail pre-foreclosure letters for us.

The RDPD meeting was in late-March, and by mid-April I had looked at several properties. I say “I” because my son was away at school. I made offers on a few of the properties – all lowball offers – but no bites. At Easter, Brenton came home for a break, and we spent a Saturday looking at several multi-families with Lisa.

Property #1 had a lady who “hated the neighborhood, and wouldn’t go outside – day or night” as well as a guy who wandered around mumbling “dust, dust, there is too much dust in the world”. He had actually taped plastic to the ceilings in his apartment to keep the dust away! The house was in rough shape, so we walked.

Property #2 had a lovely blue tarp roof. We couldn’t get into any apartment except one. The lady in that one loved the place. She also explained that everyone in the building was a little nervous about opening doors, ever since the DRUG RAID the night before. She said they took one of the tenant’s boyfriend away, along with drugs and guns. Adios, property #2!

The next place we looked at was a property at 20 Doubleday Street. This was an older 5-family with an asking price of $114,900. When we went through the apartments, they were all neatly kept. The tenants seemed happy to be there. One tenant had been there for 43 years! There were 5 gas meters and 5 electric meters! It was fully rented! BINGO!

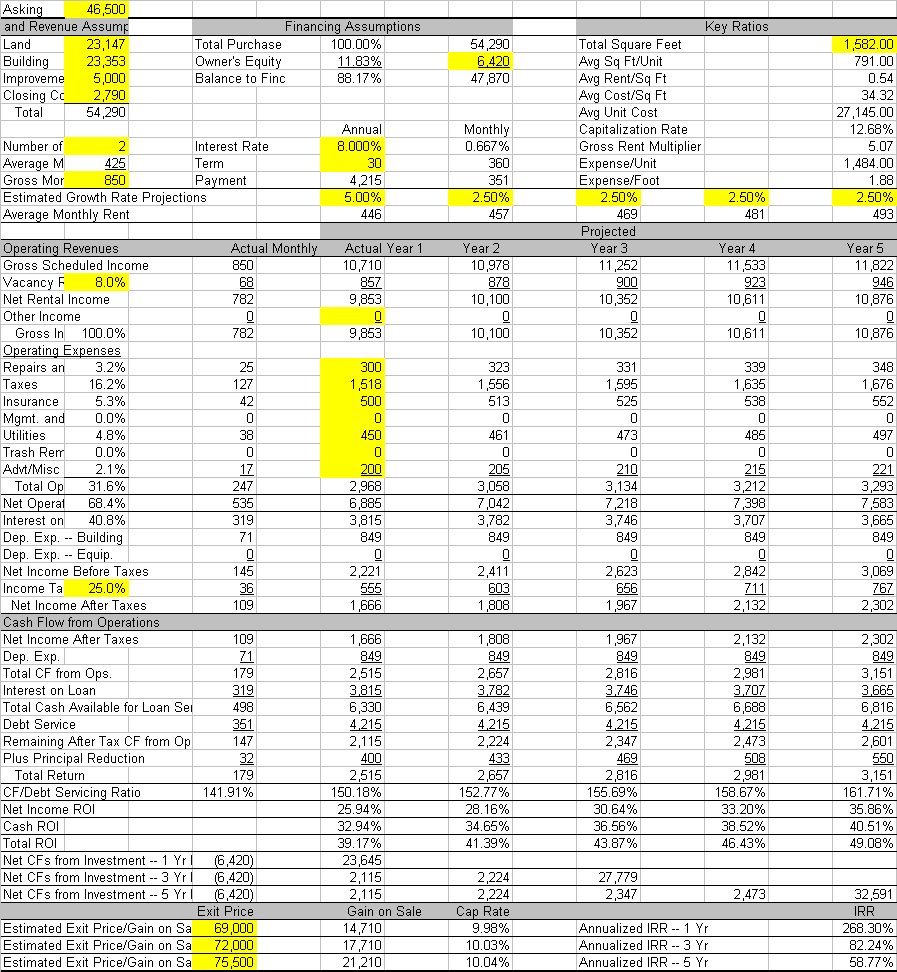

So we ran home, and put together an offer. Here were the numbers they listed in the MLS:

Annual Rents -- $26,220

Taxes -- $3,534

Insurance -- $1,358

Heat -- $5,400 (Hey! What about those separate meters?)

Electricity -- $1,168 (Again!)

Water/Sewer -- $775

Cap Rate – 12% as listed

No vacancies. No maintenance. No management.

So I sent the realtor an email. It was sort of a “Letter of Intent”, although I didn’t call it that. I made allowances for 8% vacancy, an increase in taxes, a big increase in utilities, and some room for maintenance. This brought the cap rate down to 8.63%. I made an initial offer of $90,000.

The seller came back with a $100,000 counteroffer. We asked if they would be interest in seller financing. They said “no”, but we came back with the following counteroffer anyway:

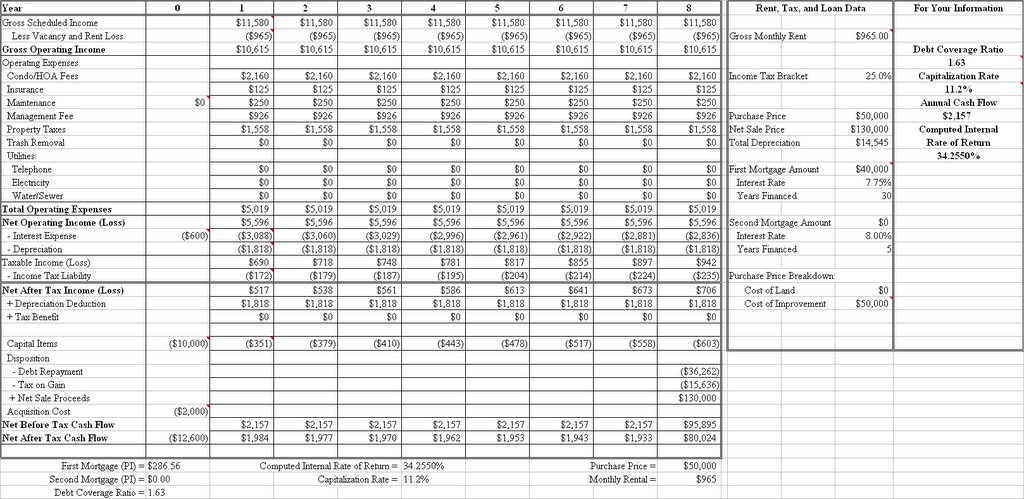

1. The first option would be an offer of $95,000** with conventional financing at 80% of the purchase price. We would pay cash for the remaining 20% of the purchase price. This would eliminate the need for seller financing.

2. The second option would be an offer of $97,500** with conventional financing for 80% of the purchase price. We would require the seller to finance the remaining 20% of the purchase price in the form of a 2nd mortgage. The terms for this financing would include us paying the seller 3 points (approx $3,000) on the purchase price at closing, with the 2nd mortgage paying interest at 8% fixed, over a term of 15 years.

3. The third option is an offer of $100,000** with conventional financing at 70% of the purchase price. We would pay 10% in cash at the time of closing. We would require the seller to finance the remaining 20% in the form of a 2nd mortgage. The terms for financing this option would be 0 points paid to the seller at closing, with the 2nd mortgage paying interest at 8% fixed, over a term of 15 years.

** All of the purchase prices outlined above will be increased to cover closing costs. All closing costs are to be rolled into the financing (subject to approval of conventional lender).

The seller quickly accepted option #2, and we signed a contract. I sent it on to my attorney, who read it and said “did you really mean to offer $3,000 plus 8% to have them finance less than $20,000???”

A call to Lisa got us out of this one – sort of. We agreed to go with option #1, but the seller getting $98,500 instead of $95,000. A $3,500 mistake, but still not a bad deal.

Lesson #2 – Have someone with good business sense proof-read your offers before they go out. Of course, I only meant to offer 3 points on the portion they were financing, not the entire purchase price LIKE I WROTE IN THE FREAKING CONTRACT!!!

We updated the terms in the contract, and faxed them off to Rochester for my son’s signatures. Things were looking good now. We’d own the place soon, and my son could work all summer long on fixups, as well as getting some landlording experience.

Doubleday is a short street, only about a block long. There are several multi-families on the block. I ask Lisa to contact all the owners to see if any others are interested in selling. She does, but no one is.

We had a property inspection done, which found a few critical items the seller had to fix, along with a list of things Brenton could do during the summer. Our lender reviewed the numbers and supporting documents, and said we got a great deal. And then things seemed to stall. Among the problems we ran into were:

The loan officer at the lender I was using had an opportunity to move to another branch. She just sort of quit replying to my calls. After a couple of weeks, we discovered what was up, and were given a temporary contact at the bank. Of course that person did nothing. Lesson #3: Be more proactive in communication.

Our attorney seemed to quit communicating with the seller’s attorney who seemed to quit communicating with the lender’s attorney. Information and documents just didn’t seem to flow from one to the other. Lesson #4: Collect all the data and documents myself, and make sure they get to the proper people.

Every time I had a question for the seller, I had to call Lisa, who had to call the seller’s agent who had to call the seller for an answer, who called Lisa, who called me. Way too many intermediaries. Lesson #5: Meet face-to-face with the seller early in negotiations, and contact them directly with questions.

Then comes June 2006, and major flooding here in Upstate NY. Fortunately, nothing happens at the property, but the area comes to a halt. Banks, hotels and hospitals are flooded. Roads are flooded or washed out. Many homes are washed away or ruined. Later, this is called a 500-year flood. This is after many people just recovered from 2005’s 100-year flood. Lesson #6: Sometimes, when you think that things “can’t get worse”, they do.

In late June, I meet my new loan officer. Nice guy. He’s new to the bank, and is going on vacation next week. Lesson #7: See lesson #6.

I’ve grown concerned with the idea of having to sell many of my stocks to finance the 20% down payment. I have a lot of gain in these stocks, and I’d prefer not to pay taxes on those gains. So, I hatch an idea to use the account as collateral for a line-of-credit at the bank. I’m told that they can do this “with no problem”. “How much do you want”, they ask. I say $50,000. They say $35,000. OK, I’ll take it. Lesson #8: There really is more than one way to skin a cat!

Mid-July hits, and I’m told we should close on the 21st! I wait and wait, but no call from my attorney with a final date and time. Finally, I receive an email stating that he is waiting for approval from the lender’s attorney and that he somehow missed getting the Certificate of Occupancy and Certificate of Compliance from the seller. Looks like no closing for a few days at least.

July comes and goes. Still no closing date. I call and email my attorney. He says that the bank has required a survey, since this is a commercial property (over 4 units). He’ll take care of that. But the lender’s attorney is only in the office on a limited schedule. His wife is having twins, and has gone into the hospital with complications. Lesson #9: Always require full physicals of attorneys and their immediate families.

Shortly after this, the wife delivers the twins prematurely. She is doing OK, but the infants aren’t in such great shape. The lender’s attorney will be out of the office for the foreseeable future. They assign a new attorney to the case. She leaves for vacation the next day. Lesson #10: Those jokes about attorneys…they aren’t really jokes. I’m thinking about how a batch of them might taste “with Fava beans”.

The new attorney returns. I know this because I receive a short email from my attorney. It says, “bob-got letter from bank's lawyer asking for all kinds of stuff. need to talk. will track you down.” In all reality, the attorney didn’t need all that much. The prior attorney had most of it, but she just didn’t know it yet. Closing day is drawing near! Unfortunately, so is the date that Brenton has to return to college. I’m assured that we’ll close before then.

Somewhere during all this, I called my insurance agent to secure insurance for the new property. He comes back with “about $2,800”, but he isn’t sure how quickly they can firm up the quote. Mind you, the seller listed insurance at $1,358! I call Lisa, who calls the seller’s agent, who…well, you know the rest. She gets the name of their insurance company. I call them, and lock in insurance, with no inspection, at $1,582. This is based on a higher replacement value than the seller had. Lesson #11: Get insurance quotes early, and shop around.

It’s August 9th, and we’re at my attorney’s having Brenton sign Power-of-Attorney forms because he has to go back to college in the morning and we still haven’t closed. While I’m there, I pick my attorney’s brain on a Short Sale deal I’m working. There is a bankruptcy involved, and he gives me a few warnings about potential problems. Lesson #12: Never put the Fava beans in before you are done picking an attorney’s brain.

Shortly after this, I get a call from the bank. They have received a letter from Schwab stating that they will not allow the account to be pledged as security. I call them, and find out that they require $1,000,000 in equity and no margin before they will consider this. I have neither. I call the bank, and argue my case. They mull things over for a day before coming back with a solution. They will still give me a line-of-credit for the same amount, but I’ll need to give them a second mortgage. Lesson #13: Be persistent. Stubbornness will yield you great benefits.

August 22nd is closing day! I hang up and call them right back, just to make sure I am on with the right attorney. In the time since my first walk-through, a tenant has left. When I talk to Lisa to firm things up (we were planning on some repairs to that apartment, plus a furnace conversion), I find out that it has been re-rented to a couple displaced by the flood. And this is at an increase in rent!

The day of the closing, I do another walk-through, this time with both Lisa and the seller. Everything is in great shape. In fact, he has put in some new electrical in the basement. The apartments are all still spotless! Where did these tenants come from???

The morning before of the walk-through, I look through the legals in the local paper. 40 Doubleday is in foreclosure. During the walk-through, I look at the property next door (22 Doubleday). It is a similar structure, although not maintained as well. The seller says that someone just bought the place a year ago, a he died recently. Hmmmm???

I go home, and do a quick search on the MLS. A 2-family at 44 Doubleday – the last house on the street – is for sale. A check the next morning finds a 3-unit (2 houses) at 14 Doubleday is for sale. Both of these were bought by out-of-area buyers within the last year. 14 Doubleday got a new roof before the owner decided out-of-town remodeling was too hard.

So…I’m looking at all these places next Wednesday. Before things are done, we may own the better part of the block! These places were all bought real cheap by the last owners, so I’m hopeful I can work some seller financing on them. I may be open to partnering with someone too. If you’re interested, drop me an email at Bob@HomeProRentals.com – just put Doubleday in the subject line or I may delete you.

Lesson #14: Never, ever, ever, give up! The seeds you plant in your daily dealings will eventually grow.